Despite record levels of deployment of new cash in deals through Q3 2021, the Private Capital Markets remain in a state of excess liquidity.

Credit funds, such as BDC’s, continue to be an important source of financing for middle market companies and PEGs.

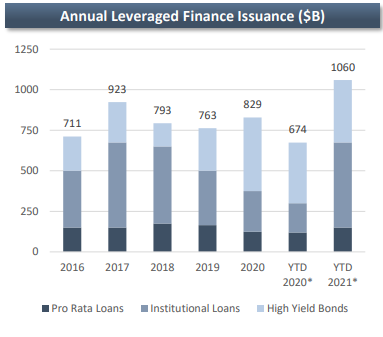

Through Q3 2021, leveraged loan volume was ~$935 billion with ~$389 billion in high yield volume

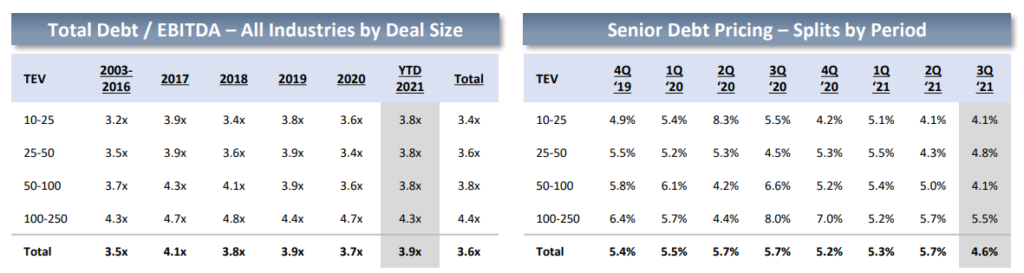

We’ve seen a return to pre-pandemic pricing and leverage levels.

In Q4, investors have historically been able to be more selective in environments with such frenzied activity, the sheer level of capital available for deployment this year is going against this historical trend.

Pricing & Leverage Trends

Borrowers generally believe that their constraint on leverage is their own risk tolerance, not the limitations of lenders.

Pricing levels have continued to tighten to pre-pandemic levels, coinciding with leverage levels rising as investors look for more opportunities to put excess capital to work.

Leverage remained at pre-COVID levels in Q3, continuing a progression from Q1 and the latter half of last year.

Overall, total debt averaged 3.8x for the quarter, with senior debt accounting for 3.3 turns of leverage.

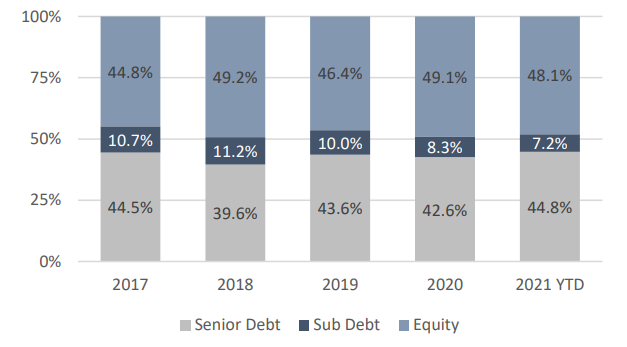

Equity and Debt Contribution by Year

Equity contributions to deals remain high as buyers position companies for growth and higher valuations create capital holes that are filled by equity.

Generally, a minimum of 50% equity (inclusive of rollover) is baseline for most deals, with a minimum of 30 – 35% new cash equity.

Support for more bespoke, structured equity solutions behind the debt continues (i.e., cash-pay or PIK equity instruments).

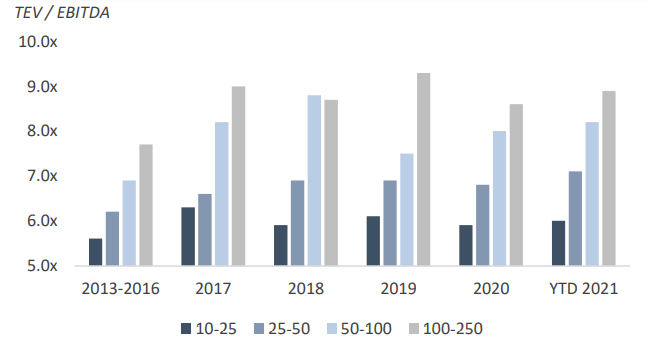

Valuation Trends

While multi-billion-dollar transactions grab the headlines, deals of $500 million and below represents 94% of deal volume over the past decade.

Transaction volumes continued to accelerate in Q3 and are expected to reach record levels in Q4.

Valuation levels remain high across the quality and size of deal spectrum.

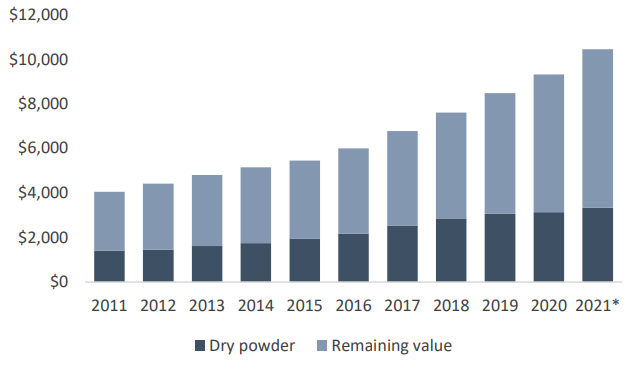

Private Capital AUM – Record Levels of Dry Powder

Across private capital, $882.9 billion was raised in the first three quarters of 2021, well on pace to exceed the full-year 2020 total.

Dry powder continues to grow with approximately $3.3 trillion of capital committed to the private markets but not deployed.