When Selling a Business, Size Matters

By: Zane Tarence

Companies are generally valued based on their risk adjusted future cash flows. Therefore as cash flows increase (bottom line), the value of the company increases. Normally companies are valued as a multiple of this bottom line, EBITDA (earnings before interest, tax, depreciation, and amortization).

If a company generates $10mm in EBITDA and is valued at $80mm, we consider this business being worth 8.0x EBITDA. Another company with a similar business model and industry with $5mm in EBITDA could expect to be valued at $40mm (8.0 x $5.0mm). However, generally we see these smaller businesses being worth a relatively smaller multiple. Maybe the second company would only be worth 7.0x at $35mm.

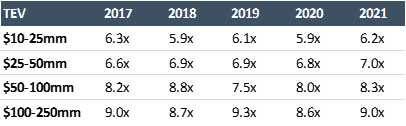

Why are these businesses considered less valuable? Shouldn’t the valuation of a smaller company be proportional to that of a large business? The table below shows empirically that larger companies are generally worth a larger multiple of their EBITDA.

Valuation Multiples by Year – Total Enterprise Value (TEV) / EBITDA

Reference: GF Data, N = 1,657

We see smaller companies are worth less (even proportionally) than larger businesses; but why?

It comes back to the first part of the valuation principal that a company is worth its risk adjusted future cash flows. Smaller companies are usually more risky than larger companies thereby requiring a larger discount. Common causes of heightened risk include:

- Revenue volatility

- Less sophisticated operations

- Less dominant market position

- Few customers and customer concentration

- And many more

We encourage business leaders to not just grow their cash flows but also develop consistency and repeatability of operations thereby decreasing risk. Being able to demonstrate consistency of operations can provide a compelling argument for a premium valuation when at the negotiation table with a buyer.